What Is an Amortisation Schedule and How Does It Work?

Are you borrowing funds? Do you understand the importance of repayments and how they are structured over time? This is where the amortisation schedule comes into play. Whether you're planning to apply through traditional banks or popular loan apps like Kissht, knowing your loan payment schedule helps you plan monthly finances efficiently.

Understanding what is amortisation is essential before taking any credit. In simple terms, it refers to the gradual repayment of a loan through fixed monthly payments over a specific period. These payments cover both principal and interest. Whether you're taking an instant personal loan or a long-term mortgage, the concept remains the same. The repayment schedule is broken down month by month in what's known as a loan amortisation schedule.

What Is Loan Amortisation?

If you're asking what is loan amortisation, it's the method lenders use to break down your EMIs. The beginning of the term has a larger portion going towards interest, while the end has more going towards the principal. Borrowers, through this method, will be able to track how their loan balance reduces over time.

Say for instance, if you take an INR two lakh instant personal loan at a 12% interest rate over a year, your monthly EMI will be calculated in a way that repays the full amount by the end of the term. Use a personal loan EMI calculator to see how much you'll pay monthly and how the interest-to-principal ratio changes.

What Is an Amortisation Schedule?

Now that we've clarified what is amortisation, let’s look at its output: the amortisation schedule. This is a table that outlines each EMI payment from start to finish. It shows how much of each EMI goes towards interest and how much reduces your outstanding principal.

An amortisation of loan gives you clarity on where your money is going. It's especially helpful if you are comparing different offers on loan apps or selecting between lenders. If you are looking at longer tenures, the loan amortisation schedule will assist you in understanding the impact of prepayments or changes in interest rates.

How an Amortisation Table Works

A standard amortisation table shows the following for each month:

- EMI amount

- Interest component

- Principal repaid

- Remaining balance

These details help track your personal loan repayment schedule efficiently. In the initial months, you would observe that a major chunk of your EMI goes towards interest and eventually, the principal portion increases. This set-up makes repayments systematic and benefits both the lender and borrower.

You can create one manually using the amortisation schedule formula, or better, rely on financial tools like the personal loan EMI calculator available on various platforms. This gives you a full EMI schedule for personal loan in seconds.

Why Amortisation Schedule Matters

The loan amortisation process may appear routine, but it holds valuable insights. Understanding your loan amortisation schedule helps:

- Plan monthly budgets

- Anticipate the best time for prepayment

- Compare different loan products

- Track interest paid for tax-saving purposes

It’s particularly important if you're managing multiple credit lines. A transparent personal loan repayment schedule avoids confusion and improves long-term planning.

Tools to Access Amortisation Schedules

Many loan apps like Kissht now integrate digital tools to simplify financial decisions. If you’re applying for an instant personal loan, these platforms often offer built-in amortisation table generators. With just your loan amount, tenure, and interest rate, you can generate a full EMI schedule for personal loan in real-time

These tools also explain the math behind the amortisation schedule formula, helping users understand their liabilities better. Instead of guessing how much interest you’ll pay or when the balance will drop significantly, use these calculators to forecast accurately.

Mid-Term Adjustments and Amortisation

One of the overlooked benefits of knowing what is loan amortisation is that it helps you evaluate the effect of any changes mid-loan. For example, if you prepay a lump sum in the eighth month of a 24-month personal loan, your loan amortisation schedule will adjust accordingly. The principal drops sharply, reducing either your EMI or the remaining tenure.

Having a clear picture of how much is saved in interest helps you decide whether part-prepayment is worthwhile. In fact, using a personal loan EMI calculator again after such a change can show how much sooner you can become debt-free.

FAQs

1.What is an amortisation schedule?

An amortisation schedule is a detailed table showing how your loan will be repaid over time, breaking each EMI into interest and principal components.

2. How does the amortisation schedule formula work?

As per the formula, it calculates monthly payments based on loan amount, interest rate, and tenure. It splits each EMI into interest and principal, ensuring complete repayment by the end.

3.What is loan amortisation and why is it important?

Loan amortisation is the structured way of paying back borrowed money in equal monthly instalments. It gives clarity on the repayment structure and interest costs.

Instant Loans at Your Fingertips

Personal Loan

Fast, hassle-free loan for your personal needs.

Business Loan

Fuel your business growth with quick approvals.

Loan Against Property

Unlock your property’s value with ease.

Credit Pulse

Boost your credit score with smart insights.

Track your credit score

Simply enter your mobile number to get a quick overview of your credit score.

Check Now

Related articles

Jun 10, 2026

Does Checking Your Credit Score Affect Your CIBIL Score?

Jun 11, 2026

How to Improve Your Credit Score Before Applying for a Loan

Jun 11, 2026

How to Download Credit Score Report for Free?

Jun 11, 2026

CIBIL Full Form Explained: Everything You Need To Know

Jun 6, 2026

Best Health Insurance for Senior Citizens in India 2026

Jun 6, 2026

Top safest cars in India: 5-Star NCAP Rated Models

Jun 9, 2026

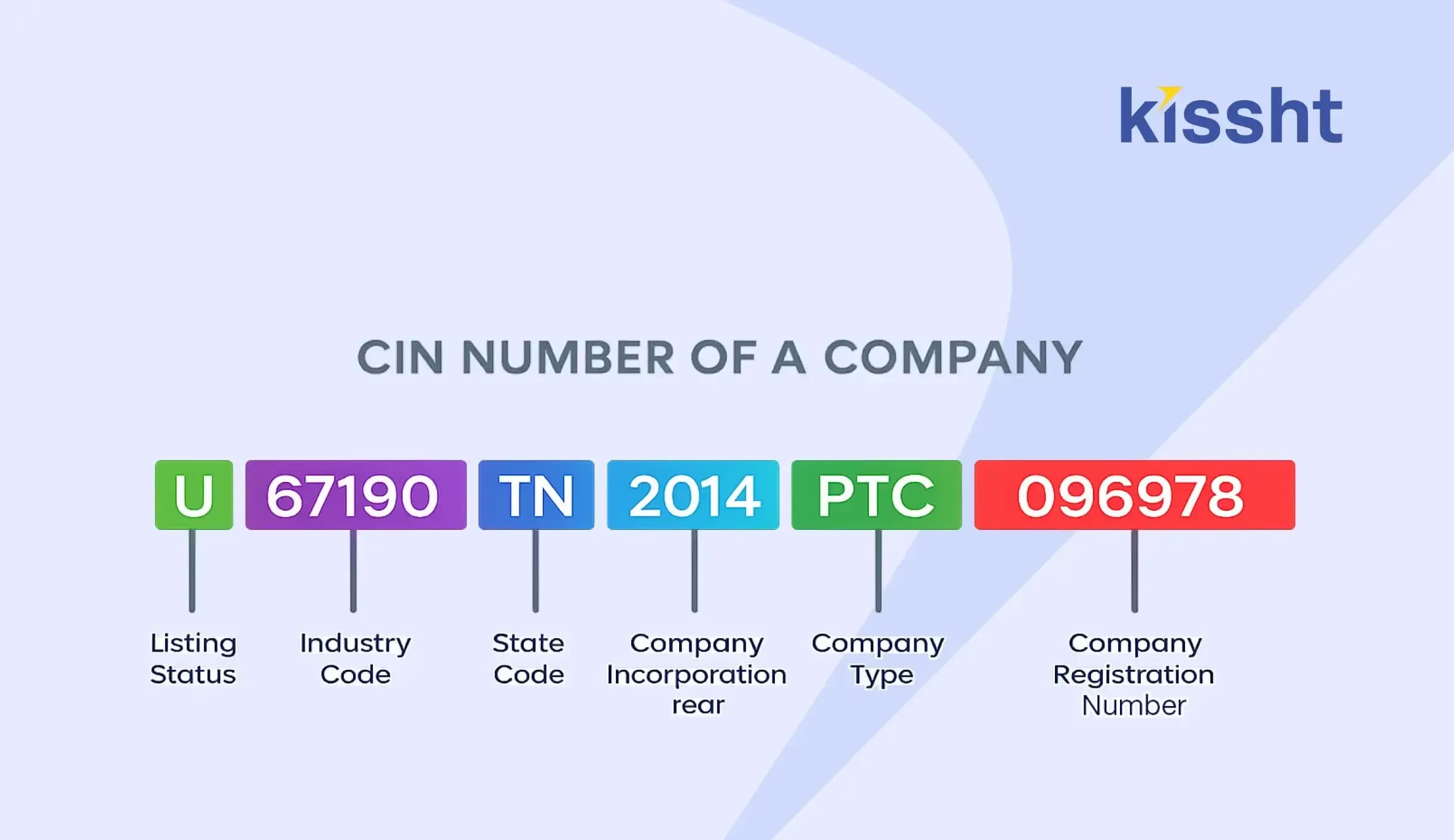

What Is CIN (Corporate Identification Number)

May 22, 2026

Learners Licence Test Questions and Answers 2026

Jun 7, 2026

Pradhan Mantri Awas Yojana Eligibility: Who Can Apply in 2026?

Jun 8, 2026

What to Gift Your Father on Father's Day 2026: Thoughtful Gift Ideas for Every Budget

Feb 23, 2026

How to Apply Electric Vehicle Subsidy in India 2026: Eligibility, Amount & Process

May 26, 2026