What Is a Debt Trap? How Young Professionals Fall into Debt

What Is a Debt Trap? How Young Professionals Fall into Debt

Managing money effectively is a key part of building financial stability, especially for young professionals at the start of their careers. With rising expenses, easy access to credit, and evolving lifestyle choices, it is important to understand how debt can impact long-term financial health.

The concept of what a debt trap is becomes relevant when borrowing starts to feel overwhelming. With easy access to credit through an instant loan app or options for an instant loan online, managing repayments becomes crucial. Using tools like a loan EMI calculator and choosing structured solutions such as a loan from Kissht can help individuals stay in control of their finances.

What Is a Debt Trap

A debt trap is a situation in which an individual takes on multiple loans or debts and struggles to repay them due to rising financial obligations.

In simple terms, a debt trap occurs when:

- Existing loans are difficult to repay

- New loans are taken to manage previous ones

- Interest keeps accumulating

- Financial stress continues to increase

How People Fall into Debt

Understanding how people fall into debt can help prevent it.

-

Easy Access to Credit

With digital platforms offering quick loans, borrowing has become more convenient. While this improves accessibility, it also requires careful financial planning.

-

Lifestyle Inflation

As income increases, spending habits often change. Unplanned expenses can lead to borrowing beyond one’s capacity.

-

Lack of Financial Planning

Not budgeting or tracking expenses can result in overspending and reliance on credit.

-

Multiple Borrowings

Taking several loans at once can lead to loan debt problems in India, especially if repayment schedules overlap.

Common Causes of a Debt Trap

Several factors contribute to a debt trap.

-

High Interest Obligations

Borrowing at high interest rates can lead to high-interest debt problems, making repayment more difficult over time.

-

Credit Card Usage

Misusing credit cards can result in credit card debt trap, especially when only minimum payments are made.

-

Irregular Income or Job Changes

Sudden changes in income can affect repayment ability.

Financial Mistakes by Young Professionals

Many financial mistakes young professionals make include:

- Not saving for emergencies

- Overestimating repayment capacity

- Ignoring interest costs

Signs of a Debt Trap

Recognising early warning signs can help avoid serious financial issues.

Common Signs of a Debt Trap

- Difficulty paying EMIs on time

- Taking new loans to repay existing ones

- Increasing dependence on credit

- Constant financial stress

Identifying these signs of a debt trap early can help you take corrective action.

Debt Trap Examples

Understanding real-life debt trap examples makes the concept clearer.

For instance, a young professional may take a personal loan for travel, use a credit card for expenses, and then take another loan to manage repayments. Over time, overlapping EMIs and interest charges create financial pressure.

This illustrates how a debt trap can develop gradually.

Role of Digital Lending in Borrowing

Digital lending platforms have made credit more accessible and convenient.

Borrowers can now:

- Apply through an instant loan app

- Access funds using instant loan online platforms

- Compare options before borrowing

While these tools provide flexibility, responsible borrowing remains essential.

Platforms offering structured repayment options, such as a loan from Kissht, can help borrowers manage finances more effectively when used wisely.

How to Avoid a Debt Trap

Understanding how to avoid a debt trap is essential for financial stability.

-

Plan Before Borrowing

Always evaluate your repayment capacity before taking a loan.

-

Use a Loan EMI Calculator

A loan EMI calculator helps you understand monthly obligations and plan your budget accordingly.

-

Limit Multiple Loans

Avoid taking several loans at the same time.

-

Build an Emergency Fund

Having savings reduces the need for borrowing during unexpected situations.

-

Track Expenses Regularly

Monitoring your spending helps prevent unnecessary borrowing.

Comparison Table: Healthy Debt vs Debt Trap

| Aspect | Healthy Debt | Debt Trap |

|---|---|---|

| Repayment | Planned and manageable | Difficult to manage |

| Number of Loans | Limited and controlled | Multiple overlapping loans |

| Financial Stress | Minimal | High |

| Borrowing Purpose | Planned expenses | Frequent or unplanned borrowing |

| Control | High control over finances | Reduced financial control |

This comparison highlights the difference between responsible borrowing and a debt trap in India.

Practical Tips for Young Professionals

- Start financial planning early

- Avoid impulsive borrowing

- Understand loan terms clearly

- Choose the best loan provider

- Prioritise savings along with spending

These habits help build long-term financial stability.

Final Thoughts

A debt trap can develop gradually if borrowing decisions aren't aligned with financial capacity. For young professionals, understanding the risks, recognising warning signs, and adopting disciplined financial habits are essential steps toward maintaining financial health. With the right approach, it is possible to use credit responsibly while avoiding unnecessary financial stress.

FAQs

Q1. What is a debt trap?

A debt trap is a situation when an individual struggles to repay loans due to increasing financial obligations and interest.

Q2. How do people fall into a debt trap?

People fall into a debt trap because of overspending, multiple loans, high interest rates, and a lack of financial planning.

Q3. What are the signs of a debt trap?

Common signs include difficulty paying EMIs, taking new loans for repayment, and increasing financial stress.

Q4. How can I avoid a debt trap?

You can avoid a debt trap by planning finances, using a loan EMI calculator, limiting borrowings, and maintaining an emergency fund.

Instant Loans at Your Fingertips

Personal Loan

Fast, hassle-free loan for your personal needs.

Business Loan

Fuel your business growth with quick approvals.

Loan Against Property

Unlock your property’s value with ease.

Credit Pulse

Boost your credit score with smart insights.

Track your credit score

Simply enter your mobile number to get a quick overview of your credit score.

Check Now

Related articles

Jun 6, 2026

Top safest cars in India: 5-Star NCAP Rated Models

Jun 9, 2026

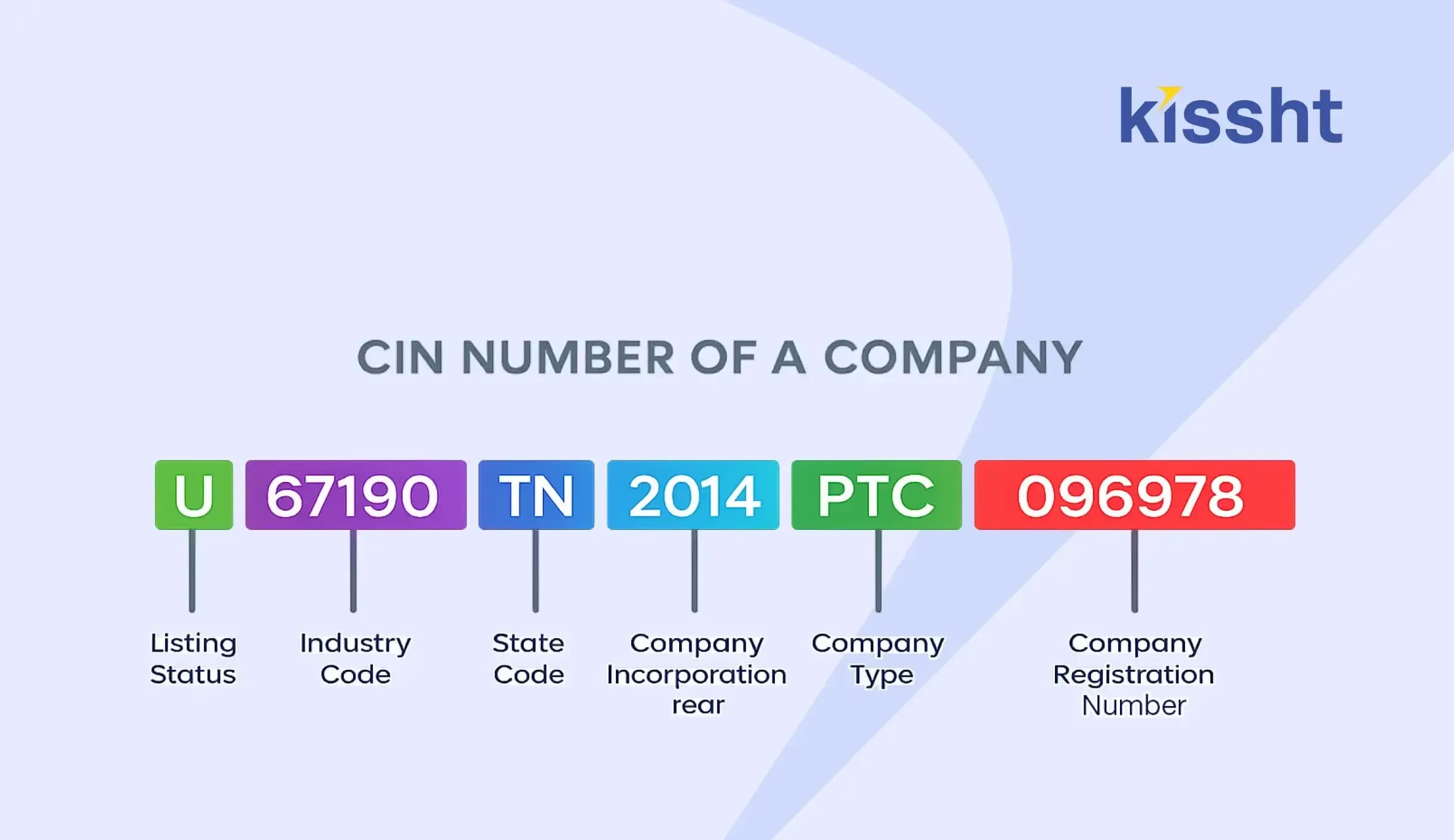

What Is CIN (Corporate Identification Number)

May 22, 2026

Learners Licence Test Questions and Answers 2026

Jun 7, 2026

Pradhan Mantri Awas Yojana Eligibility: Who Can Apply in 2026?

Jun 8, 2026

What to Gift Your Father on Father's Day 2026: Thoughtful Gift Ideas for Every Budget

Feb 23, 2026

How to Apply Electric Vehicle Subsidy in India 2026: Eligibility, Amount & Process

May 26, 2026

Diwali 2026: Date, Puja Muhurat & Lakshmi Puja Timing

May 25, 2026

Ganesh Chaturthi Holiday 2026: Date and Puja Muhurat Details

May 26, 2026

आधार कार्ड कैसे डाउनलोड करें? सबसे आसान तरीका

May 24, 2026

Money Saving Tips - List of Ways to Save Money Every Month

May 25, 2026

Best Tourist Places in India 2026

May 23, 2026